Gold Shares: Different This Time?

By David Galland

Managing Director

Casey Research

BIG GOLD

Doug Casey, my partner and Casey Research chairman, describes his secret to making life-changing investment returns – and hanging on to them — as “Being bold when everyone else is timid, and timid when everyone else is bold.”

But putting a pleasant-sounding utterance into practice is far different than just parroting it.

Especially if you have taken an interest in gold shares over the last year or so.

That’s because gold’s bull market has taken it from $691 a year ago to $918 where it trades today. That’s an increase of 33%. Yet the AMEX Gold Bugs Index has lagged and is up only 26% over the same period. (Lagged is, of course, a relative term, because the S&P 500 is down 7% over that same period.)

However, people don’t invest in gold stocks to keep up with gold… but to outpace the metal on the upside.

Case in point, before the gold bull market cooled off for a brief period in 2006, gold bullion went from its 1999 low of $252 to its 2006 peak of $725, a 187% gain. But the AMEX Gold Bugs Index went up by an even more impressive 519% over the period.

So, what’s going on in today’s market? Are gold stocks going to continue underperforming? Or is this a time to be bold and position yourself now, in anticipation of a rebound?

Is It Different This Time?

The most dangerous phrase in the investor lexicon is “This time, it’s different.” Invariably, that phrase is used to explain why an investment is going to continue in a certain mode even though history screams that just the opposite should be true.

We heard this in spades during the dot.com boom. Back then, companies with no profits and a business plan that would embarrass a high school student were valued in the hundreds of millions of dollars. “These paper tigers have to crash and burn,” said the few. “No,“ said the many, “this time it’s different because…”

The real estate bubble was no different. “But house prices have doubled and doubled again. That means you should be selling, not buying houses on the speculation that they will double yet again,” said the few. “No,” said the masses, adding, “this time it’s different because…”.

In the context of gold shares, in order for things to be different this time, the gold shares would simply flop around at current levels until the gold bull market ends. After which they would sink back to pre-bull market levels.

Could it happen? Sure. But in order for it to be different this time, the following would have to hold true.

1) Gold producers would have to realize no significant gain in profitability. That, even though the price of their primary commodity has risen strongly.

A quick check shows that, for the fourth quarter of 2007 — the last quarter for which results are available — many of the gold producers rang in record results, including Goldcorp (NYSE: GG), whose year-over-year profits almost quadrupled, and Kinross (NYSE: KGC), whose profits increased 322%. And that is just a sampling.

(As an important aside, all the big gold producers will be releasing their first-quarter financials within the next couple of weeks. Because gold reliably traded more than $100 per ounce higher over that period, compared to the fourth quarter of 2007, we expect to see another round of record-breaking financial results.)

2) One of the fundamental tenets of investing has to be chucked out of the window. That tenet is that investors gravitate to sectors where profits are on the rise. And gravitate more strongly to sectors where profit increases are strongest. With the record-breaking improvements in the gold producers’ financials of late, we can expect to see investors beginning to pile in. Especially considering that most other major sectors — financials, banking, housing, transportation, etc. – are all experiencing record losses. Indeed, if investors steer clear of the profit-making gold producers, that will be almost unprecedented.

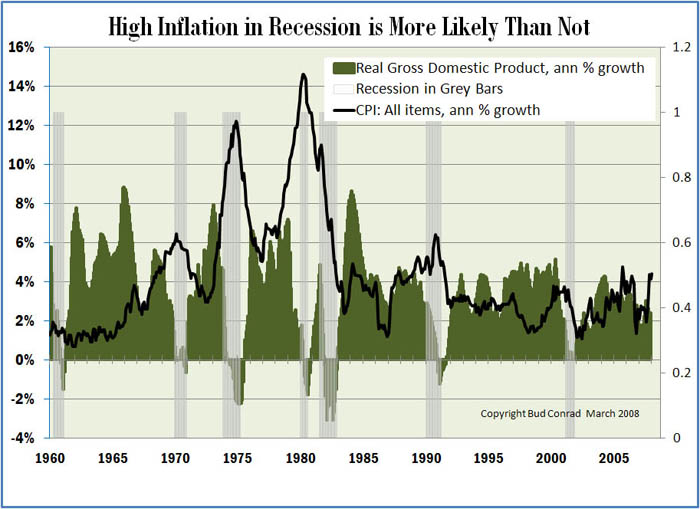

3) In a period of rising inflation, investors would have to ignore gold stocks as being a likely beneficiary. During the last major inflationary period in the U.S., 1962 to 1982, gold shares rose, on average, 1,503%. Are we in a major inflation at this point? A quick glance at any news screen or a trip to your local store will confirm that we are. Is gold no longer an inflation hedge? Again, for it to cease playing that role would be a brand-new script.

4) Gold stocks would also have to fail to trade in concert with rising oil prices. As you can see in the snapshot chart here, historically, there is a very high correlation between gold and oil.

But maybe higher oil prices are temporary, and oil will fall to meet gold, versus gold rising to meet oil? No one can say for sure, but in light of the available evidence, the safe bet would seem to be sustained higher prices.

In just the last few weeks, we have heard from the Saudis that they won’t be increasing oil production from current levels (according to many credible analysts, it is because they cannot)… and from the Russians that they may have hit peak oil production… and that Mexico, the third largest oil exporter to the U.S., will export its last barrel to the U.S. in just 6 years.

In short, for the coiled spring under gold stocks to fail to be triggered, things would indeed have to be very, very different this time around.

Raising One Final Question…

But what if the gold bull market is already over? After all, after touching an all-time high (in non-inflation-adjusted dollars) of $1,011 on March 17th, gold fell back as low as $887.75, a drop of 13.91%.

Other than scaring some investors away from gold, is that correction significant? The answer, again based on the historical record, is no. Since the gold bull market began in 2001, there have been 9 significant corrections (defined as a retraction of more than 8%). The worst of those corrections have seen gold fall 15.98%, 18.27%, and 27.7%. The average retraction of all of those corrections is 13.6%, so the latest is, at worse, fractionally worse than average. It is worth noting that we saw a very similar pattern back in the 1970s with gold stutter-stepping higher and higher.

So the latest correction, in and of itself, is truly inconsequential.

Leaving us to look elsewhere in order to answer the question of whether the gold bull market is over.

We think the answer is obvious and requires only a casual glance at the facts on the ground. We now have globally raging inflation, a financial crisis the likes of which hasn’t been seen in generations, a massive unleashing of cheap money by the Fed, a $3 trillion war and governments trapped into spending without restraint. On that last front, in addition to the almost mind-numbing financial obligations to the 78 million baby boomers now retiring, we now have a cacophony of calls for universal health care in the U.S., and the near-certainty of a new Democratic president coming into power with the mandate to deliver just that.

All of which is to say, monetary inflation is the rule of the day.

Opportunity Knocks

Per above, within the next couple weeks the big gold-producing companies are going to release their latest financials — and they are going to impress, you can be sure of that. When people compare those results against the train wrecks occurring in almost all the other investment sectors, the gold stocks story is going to shine particularly bright. And, unless this time things really are different, a bet we wouldn’t take, these eye-opening profits should soon begin to translate into investor interest that unleashes the gold stocks.

Before signing off, I’ll share a final chart, this one from a presentation James Turk (www.goldmoney.com) recently gave at one of our Casey Research Summits. It shows the historical trading range between gold bullion and gold stocks, with the measure of value being gold bullion (versus the U.S. dollar). As you can see, the XAU index of gold stocks is now right at the bottom of its trading range… and that the top of the range is about twice as high from here.

Could the gold stocks double from here?

In our view, that is the by far most likely scenario. And a scenario that we think the historical record supports. This opportunity won’t last overly long because sooner rather than later (and maybe as soon as the next wave of financials are released), the investment masses, led by the deep-pocketed institutions, are going to come to the conclusion that in this era of crisis and inflation, the single best place for their money is in gold producers. Get there first, and you’ll profit most.

David Galland is the managing director of Casey Research, LLC, publishers of BIG GOLD, a unique publication dedicated to providing actionable research on producing and near-production gold and silver companies. To learn more about our 3-month, risk-free trial offer with 100% money-back guarantee, click here.